Question then arises as to whether an individual who is not a GST registered person is required to pay GST when making a supply of his commercial property. In the service tax no input exemption mechanism is.

Malaysia Sst Sales And Service Tax A Complete Guide

If the supply of commercial residential building or premise is determined as residential property then the supply is exempted from GST.

. RPGT increases progressively as follows for commercial property. The Service tax is also a single-stage tax with a rate of 6. OVERVIEW OF SUPPLY Scope of Tax 5.

GST is to be charged and levied on. Section 9 of GST Act stipulates that tax shall be charged on any supply of goods or service made in Malaysia where it is a taxable supply made by a taxable person in the course or furtherance of any business carried on by him. If sold before 4 years.

Any individual that supplies commercial property or commercial land worth more than 2 million ringgit at market price after 28 October 2015 shall liable to register for GST. This DGs decision clarifies the GST treatments for Individual supplies commercial properties ie. GST is charged on all taxable supplies of goods and services in Malaysia unless specifically exempted.

A supply becomes taxable where the annual sales turnover exceeds RM500. This ruling is to determine whether the supply of commercial residential building or premise on commercial land will be classified as either a residential or commercial property. Payment of tax is made in stages by the intermediaries in the production and.

By 9 July 2015 we usher 100 days on from the start of GST one of the major pieces of tax reform the country has seen. For the consumers they can identify the standard rated supplies by looking at the receipt when making the purchase. Sales of commercial real estate such as office towers retail buildings and land zoned for commercial use are subject to a 6 percent GST if the seller is an individual is engaged in the business.

Whether an individual has to charge GST when making a supply of his commercial property. Contractors engineers will be subject to GST with a standard rate of 6. GST is also charged on importation of goods and services into Malaysia.

This tax is not required for imported or exported services. Malaysian businesses are required to register for GST when their turnover threshold hits RM500000. Unlike residential properties the sale of commercial properties is a clear cut case which falls under the Standard-rated supply and is taxable under the GST.

Sales of commercial real estate such as office towers retail buildings and land zoned for commercial use are subject to a 6 percent GST if the seller is an individual is engaged in the business. Sales tax and service tax will be abolished. GST is charged to a registered person.

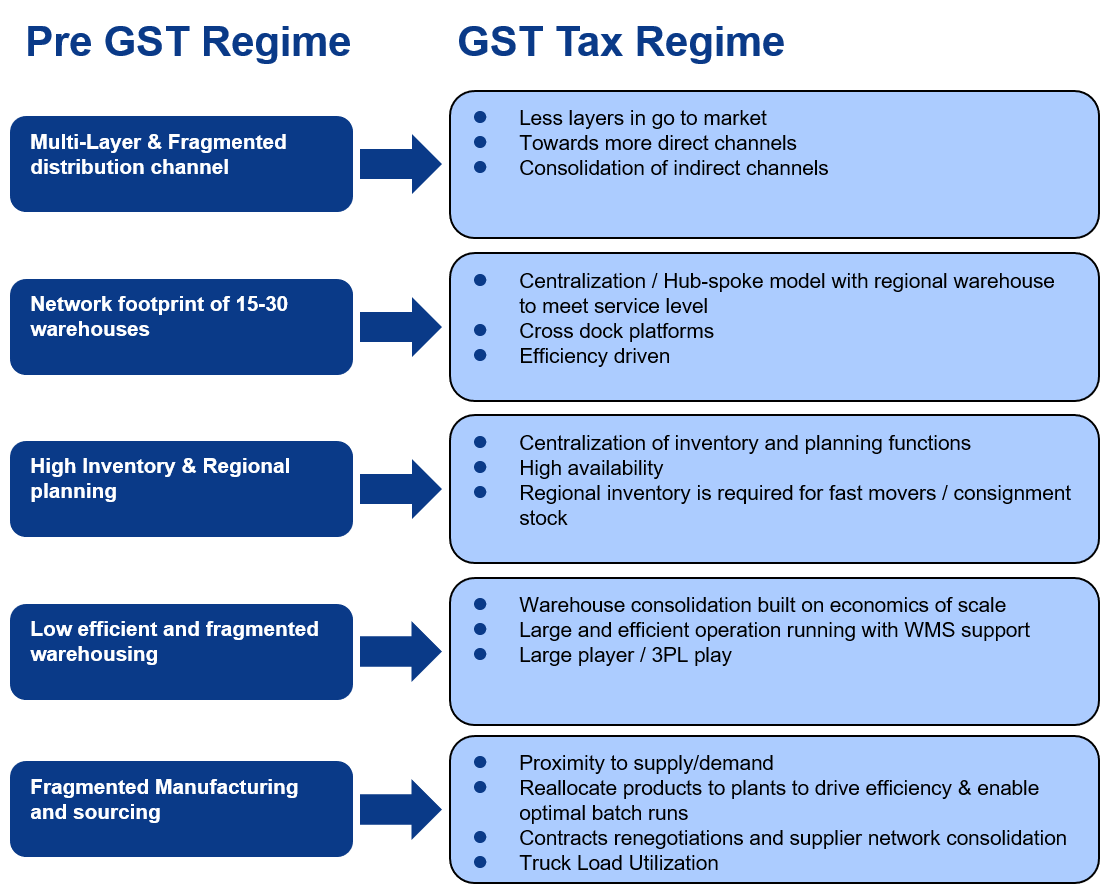

Goods and Services Tax GST is a multi-stage tax on domestic consumption. Item 2Supply of commercial property build sell by the developer to the purchaser under an agreement for a period that begins before the effective date and ends on or after the Item 3Eligibility for deemed Input Tax under Regulation 47 of. This article looks at some of the significant impacts GST has brought.

Goods and Services Tax GST Malaysia will be implemented with effective from 1 April 2015 and GST rate is fixed at 6 per cent. Whether an individual has to charge GST when making a supply of his commercial property. The examples of standard rated supplies are local supply of goods or services supply of land and building for commercial and construction of all types of building.

If sold after 6 years. Is GST Chargeable When Making a Supply of Commercial Property. If sold before 5 years.

Property is located in Malaysia. Any individual that supplies commercial property or commercial land worth more than 2 million ringgit at market price after 28 October 2015 shall liable to register for GST. Panel Decision 4 Author.

Any late registration will be subject to penalty based on number of days late which capped at RM20000. Keep in mind that tax rates change frequently and you should check the latest government information for up-to-date data. The Decision 4 2014 made by the Director General of the Royal Malaysian Customs as amended with effect from 28 October 2015 provides more clarify on this point.

Under the new GST implementation all building materials and services Eg. The current regulations might confused a lot of people who originally thought they were exempt from this levy according to Deloitte Malaysia an. The current regulations might confused a lot of people who originally thought they were exempt from this levy according to Deloitte Malaysia an.

GST will not be imposed on piped water and first 200 units of electricity per month for domestic. A any supply of goods or services made in Malaysia including supply of imported services and anything treated as a supply under the Act. Individual supply commercial property i on any taxable supply of goods or services made in Malaysia section 9 GSTA.

If sold within 3 years. Whether the supply made is a taxable supply. This will invariably raise the production cost.

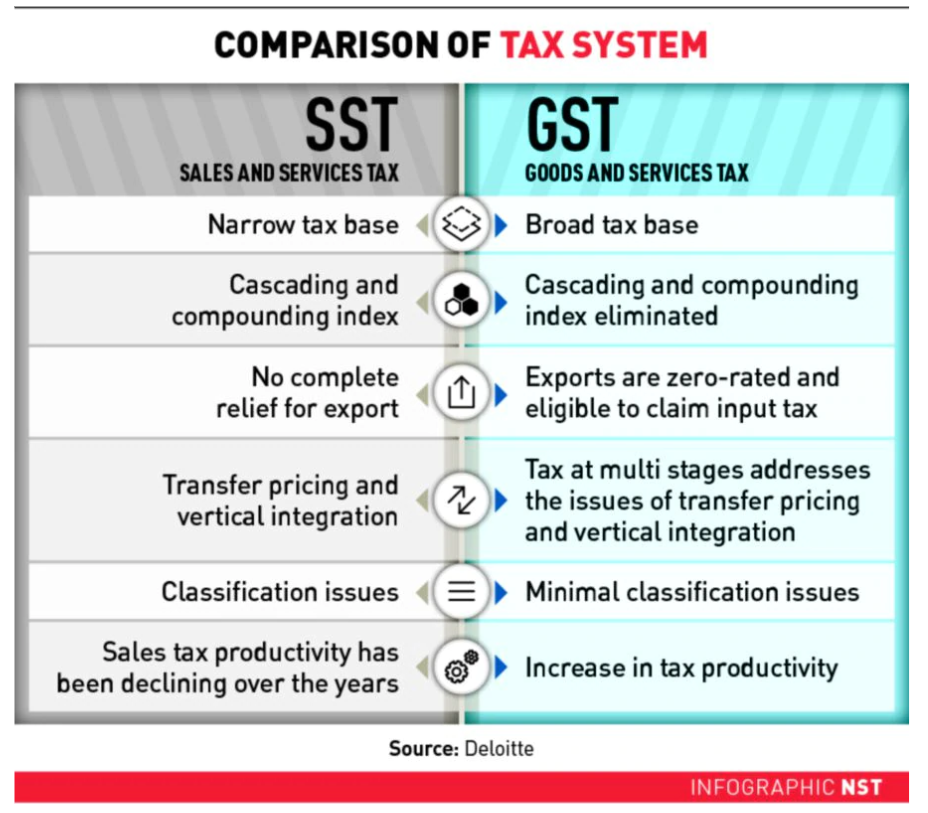

Goods and Services Tax GST is a multi-stage tax which replaces the Government Sales Tax and the Service Tax. As one of the most sophisticated sectors undoubtedly property and construction industry faced greater challenges in complying with GST rules. Late Registration Period Days Cumulative RM 1 30.

Currently Sales tax and service tax rates are 10 and 6 respectively. And b any importation of goods into Malaysia. Normally standard rated supplies GST labelled with an S.

GST is charged on all taxable supplies of goods and services in Malaysia except those specifically exempted. GSTA section 2 of the current month and the next eleven months exceeds RM500000 GST shall be charged by a taxable person in the. A person is liable to registered if his total taxable supply of the current month and the next 11 months exceeds Rm500000.

Service Tax is charged on a specific service provided by a taxable person in Malaysia carrying out a business. Whether an individual has to charge GST when making a supply of his commercial property. Custom Malaysia has updated the DGs Decision 42014 Item 6 and the amendments were effective from 28 October 2015.

GST is charged on any supply of goods and services if the following. In determining this threshold income arising from the supply of capital assets of the business which was previously excluded will now fall within the RM500000 threshold unless the capital assets are supplied or transferred as a result of the cessation of. Ii Taxable person means any person who is or is liable to be registered under section 2 GSTA.

Any individual owning commercial property at any one time-Make a supply of two commercial properties or commercial land not exceeding 1 acre would be treated as not carrying out business. Meanwhile other building materials fall inside Second Schedule Goods in which all the goods in this category will only be charged sales tax of 5. GST shall be charged by a taxable person in the course or furtherance of business on any taxable supply of goods or services made in Malaysia section 9 GSTA.

Profit And Loss Report Web Based Online Accounting Software Malaysia Online Accounting Softwa Online Accounting Software Accounting Software Create Invoice

The Serious Research Gap On Vat Gst A New Empcom Gov In

Gst B200tj 1a Casio

Recombinant Anti Gst3 Gst Pi Antibody Epr8263 Ko Tested Ab138491 Abcam

What Is The Gst Tax

When Should A Business Apply For Multiple Gst Registrations All One Needs To Know Ipleaders

India S Tax Reform Its Impact To Supply Chain

2

Gst B200tj 1a Casio

Construction Quotation Template 20 For Word Excel Pdf Quotations Quotation Sample Quotation Format

Pdf Goods And Services Tax Gst Transition To Sales And Services Tax Sst Impact On The Welfare Of B40 And M40 Households In Malaysia

Anti Gst3 Gst Pi Antibody Ab153949 Abcam

Pdf The New Zealand Gst And Its Global Impact 30 Years On

Gst B200tj 1a Casio

Supply Under Gst

Gst B200tj 1a Casio

Navigating The Gst Rate Hike

Letter Head Of The Construction Company Letterhead Design Company Letterhead Visiting Card Design

Anti Gst3 Gst Pi Antibody Ko Tested Ab117885 Abcam